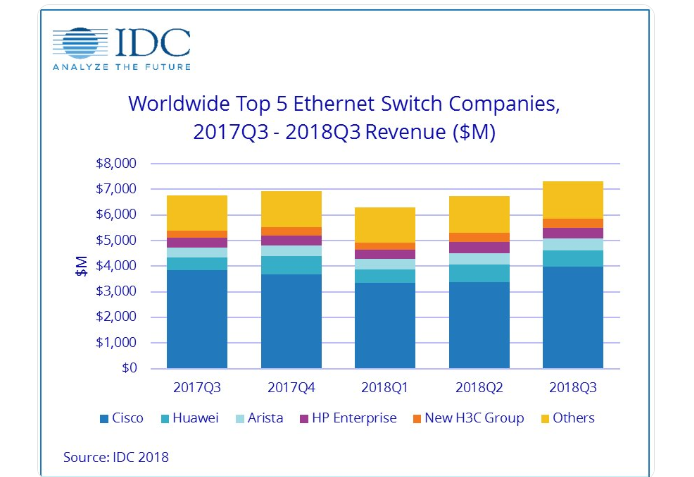

The Worldwide Ethernet switch market (Layer 2/3) recorded $7.3 billion in revenue in 3Q18, an increase of 8.1% YoY, while total enterprise and service provider (SP) router market revenues declined 5.1% YoY in 3Q18 to $3.7 billion, according to IDC's Quarterly Ethernet Switch Tracker and IDC Quarterly Router Tracker.

"Digital Transformation and adoption of Third Platform technologies continue to drive demand for network transformation and in turn the Ethernet switching equipment market," said Rohit Mehra, vice president, Network Infrastructure, at IDC. "While hyperscalers and cloud service providers are pushing consumption at the high end of the switching market, there remains strong growth in the enterprise campus and lower speed switching platforms too, highlighting the increased demands of the network from organizations of all sizes."

Some highlights from IDC:

- 100Gb Ethernet switch revenues continue to grow rapidly. Port shipments for 100Gb switches rose 154.6% year over year to 3.5 million.

- 100Gb revenues broke the $1 billion barrier in 3Q18, reaching $1.1 billion to make up 14.8% of the market's total revenue.

- 25Gb ports saw even higher growth rates with port shipments up 251.0% to 2.6 million and revenue increasing 219.6% year over year for 3.7% of the market's revenue.

- 40Gb port shipments rose too, growing 12.6% year over year to 1.3 million, while revenues declined 10.4% for 7.5% of the market's total.

- Lower-speed campus switches continued to see strong demand.

- 10Gb port shipments rose 16.0% year over year to make up 28.8% of the market's revenue.

- 1Gb switches saw port shipments grow 8.4% year over year to 116.4 million, representing 42.3% of the market's total revenues.

- The worldwide enterprise and service provider router market fell by 5.1% on a year-over-year basis in 3Q18 with the major service provider segment, which accounts for 76.2% of revenues, declining by 7.3%.

- The enterprise portion of the router market grew 2.5% year over year.

- From a regional perspective, the combined service provider and enterprise router market declined 24.4% in the U.S., where service provider revenues dropped 31.5% while enterprise revenues grew 8.7%.

- Cisco finished 3Q18 with a 3.8% year-over-year increase in overall Ethernet switch revenues and market share of 54.4%. In the hotly contested 25Gb/50Gb/100Gb segment, Cisco is the market leader with 39.4% revenue, which is up from the 34.6% share it held in this segment in the previous quarter. Cisco's combined service provider and enterprise router revenue declined 2.2% year over year, with enterprise router revenue increasing 4.1% but service provider revenues declining 5.3%. Cisco's combined service provider and enterprise router market share increased to 42.7% from 35.7% last quarter.

- Huawei's Ethernet switch revenue rose 21.3% on an annualized basis but was down 7.5% sequentially from 2Q18 to 3Q18 with market share of 8.6%. The company's combined service provider and enterprise router revenue rose 2.2% year over year with a market share of 23.5%.

- Arista Networks saw Ethernet switch revenues increase 27.6% in 3Q18, bringing its share to 6.6% of the total market, up from 5.6% a year earlier. With its focus on the datacenter, the company continues to cater to the higher end of Ethernet switch speeds with 100Gb revenues accounting for 66.1% of the company's total revenue, indicating the company's focus on cloud providers and large enterprises.

- HPE's Ethernet switch revenue grew 12.0% year over year but was off 4.9% sequentially. The company's market share rose to 5.7%, up from 5.5% a year earlier.

- Juniper's Ethernet switch revenue grew 3.8% in 3Q19, bringing its market share to 3.0%. Juniper saw a 15.2% decline in combined enterprise and service provider router sales, bringing its market share in the router market to 13.4%.