China Mobile, the world's largest mobile operator in terms of customers, published a mixed report for the first half of 2018, revealing increased profitability amidst an overall drop in revenue, heightened price competition from rivals China Telecom and China Unicom, and a slowing of new customer additions as the market becomes saturated even in rural areas of the country. It is a mixed picture as well because China Mobile is seeing a wave of IoT activations of its network, as well continued triple-digit growth in handset data traffic, yet tighter cost management and better efficiency are touted as the path forward. China's central government has pressured the Big 3 operators to speed up their network upgrade programs, while at the same time imposing tariff reductions, especially the cancellation fo domestic data roaming tariffs between provinces. China Mobile retains a 53% market share, making it the strongest of the Big 3

In terms of revenue growth, voice revenue is eroding at an alarming rate (-6.4%) due to the tariff reductions; SMS and MMS are flat (+0.1%); wireless data revenue is the bright spot (+7.0%) but far outpaced by traffic growth of 153%; and wireline broadband is expanding at rate more typical for developed markets (+2.5%).

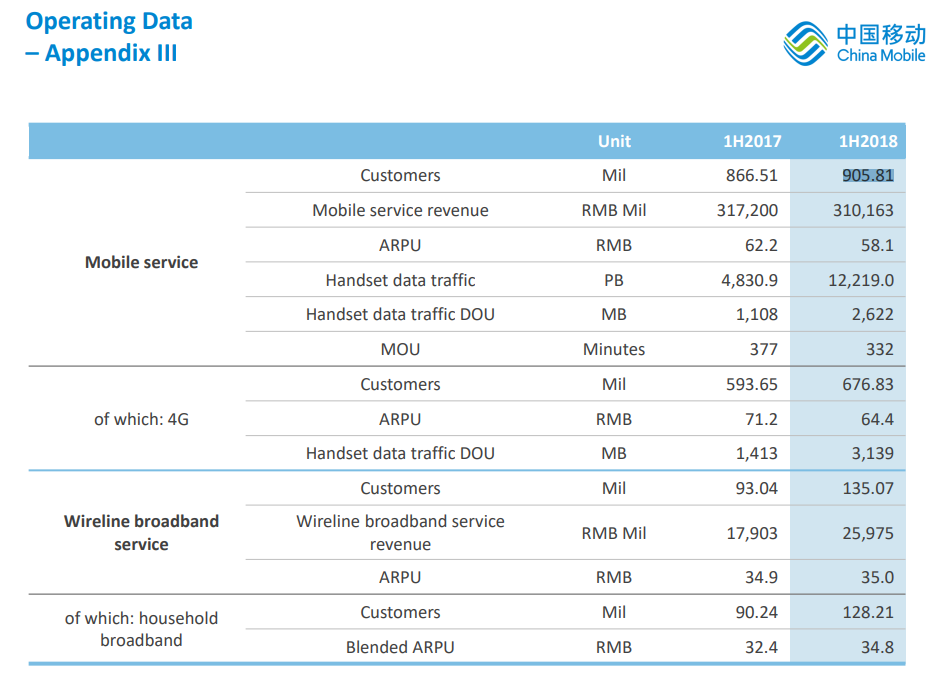

Operating data published by China Mobile (in English) for the first half of 2018 is extensive, more so than the quarterly data disclosed by major operators in western countries, which is surprising as one might expect the opposite to be true.

Unlike the big three U.S. operators who enjoy ARPU is the US$50+ range, China Mobile must make do with ARPU of RMB 58.10 (US$8.43) -- about 1/6th the billing per subscriber per month -- a. China Mobile is clearly gearing up for what is likely to be one world's fastest and deepest rollouts of 5G. They are already known for running a tight ship in terms of cost management. To complete this 5G upgrade cycle they are promising to cut costs even further. And while China Mobile has a very large number of employees, individual salaries are low compared to western peers and so automation of network administration functions may not have as big a payback, which will mean that efficiency gains will have to come from somewhere else.

Unlike the big three U.S. operators who enjoy ARPU is the US$50+ range, China Mobile must make do with ARPU of RMB 58.10 (US$8.43) -- about 1/6th the billing per subscriber per month -- a. China Mobile is clearly gearing up for what is likely to be one world's fastest and deepest rollouts of 5G. They are already known for running a tight ship in terms of cost management. To complete this 5G upgrade cycle they are promising to cut costs even further. And while China Mobile has a very large number of employees, individual salaries are low compared to western peers and so automation of network administration functions may not have as big a payback, which will mean that efficiency gains will have to come from somewhere else.The semi-annual report gives us a good idea of where China Mobile intends to cut. Its cost cutting targets include:

-15.4% -- average maintenance expense per base station

-7.5% -- average power and utility expense per base station

-9.0% -- average selling expense per new additional customer

-0.13pp -- operating lease charges to revenue

A lot of these expenses are associated with the physical infrastructure that was handed over to China Tower, which completed its IPO in a Hong Kong listing only last week. China Mobile's new report states that tower leasing fees cannot exceed the budget established at the beginning. And now there are these new expectations for reduced maintenance, as well as expectations for the 5G rollout and network densification.

Top and bottom lines for 1H2018

Profits at China Mobile are growing, even if other aspects of the business are under challenge. EBITDA grew by 3.7% compared to the same period last year, reaching RMB145.9 billion. Profit attributable to equity shareholders grew by 4.7% year-on-year to RMB65.6 billion. While overall review was down, operating revenue of RMB391.8 billion, up by 2.9% compared to the same period last year, and telecommunications services revenue was RMB356.1 billion, up by 5.5% compared to the same period last year.

The Four Growth Engines

With its 906 million mobile customers, it is clear that this is the engine that really matters.

The total number of connections increased to 1.425 billion, comprising 906 million mobile connections, 135 million wireline broadband connections and 384 million IoT connections.

In the first half of 2018, the average handset data traffic per user per month, or DOU, of 4G customers exceeded 3GB while the total handset data traffic increased by 153%, while revenue for data traffic grew 15.3%. Actually, for Q2, data traffic grew 164%, so we are likely to see and even bigger data traffic growth rate for the rest of 2018. So far, China Mobile has managed to move 75% of its users onto the 4G network.

Revenue for the personal mobile market grew by only 1.1% compared to the first half of 2017.

In fixed line residential Internet service, China Mobile is adding customers at a good clip and its market share has now reached 39% with 128.2 million households. This is bad news for China Telecom and China Unicom. Net growth in household broadband customers reached 18.80 million, accounting for 57% of the total number of net additional customers in the industry. Over 42% of households receive over 100 Mbps connection speeds, a strong showing compared to many developed countries. Household ARPU is also rising (+7.2% yoy) although ARPU remains at a very low level RMB 35.0 (US$5.08).

In the first half of 2018, application and information services revenue grew by 23.5%.

China Mobile also said it is rapidly completing a national NB-IoT network, which it expects to launch before the end of the year.

China Mobile's total number of IoT smart connections has reached 384 million and revenue from IoT business recorded a year-on-year growth of 47.6%.

The CAPEX story

For 1H2018, China Mobile spent RMB 79.5 billion (US$11.54 billion), down from RMB 85.3 billion for 1H2017. For the full 2018, China Mobile anticipates total CAPEX will be RMB 166.1 billion, down from RMB 177.5 billion for all of 2017.

For comparison, Verizon's CAPEX for 1H 2018 was $7.8 billion, compared to $7.0 billion for 1H 2017. Deutsche Telekom listed its 1H2018 revenue at EUR 6.1 billion for "both sides of the Atlantic."

The CAPEX budget for 1H2018 was as follows:

- 36.7% - Mobile communications networks, including the addition of 190,000 4G base stations

- 37.6% - Transmission networks

- 10.7% - Business networks

- 4.4% - Support systems

- 8.3% - Buildings & infrastructure & power systems

- 2.3% - Other

The 5G plan

China Mobile has been granted an LTE FDD (Frequency-Division Duplexing) operating permit and says it is working to speed up network convergence.

The operator plans 5G trials for the remainder of 2018. The corporate report states: "The development of 5G bears great significance to the Company for its profound implications on our sustainability... We are keen to generate returns on our investments and will plan our future investments on 5G taking into consideration the level of maturity of the industry and business models that emerge"

China Mobile awards EUR 1 billion deal to Nokia